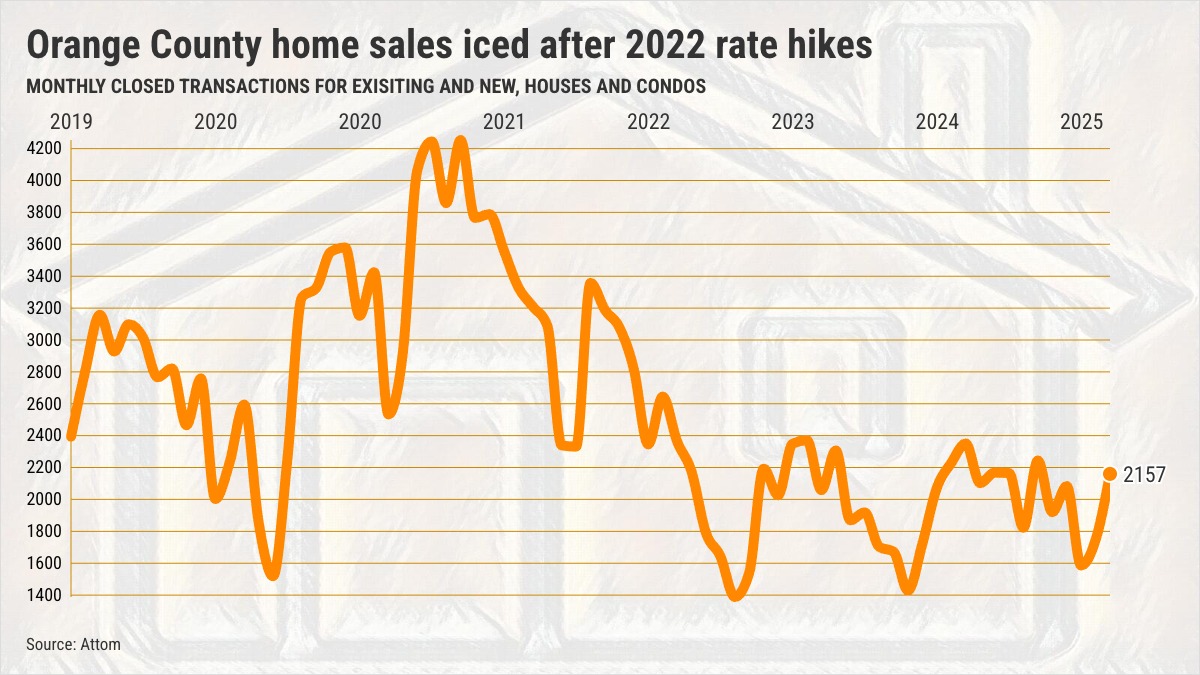

Orange County homebuying hasn’t been the same since the Federal Reserve’s war on inflation began three years ago.

That’s what my trusty spreadsheet revealed in the March homebuying report from Attom, which tracks the closed sales of existing residences and new construction, including houses and condos, dating back to 2005.

The Fed’s efforts to cool an overheated economy with pricier financing began in March 2022. It totally iced home sales.

For example, March 2025’s 2,157 sales were the third-smallest total for the month since 2005. It’s also 27% below the month’s 20-year average.

Or take a longer-term view of homebuying’s collapse.

In the 36 months since the Fed started its cost-of-living focus, 2,087 Orange County residences were sold in the average month vs. 3,031 in pandemic-twisted 2019-22.

We’re talking a 31% plummet that’s also 23% slower than the 20-year average.

The price is wrong

When the pandemic upended the business climate, the Fed came to the rescue with cheap money, and home prices surged.

Then, numerous stimulus efforts and supply shortages boosted inflation to a four-decade high. The central bank ended its cheap money party, and yet Orange County home prices did not reverse.

Contemplate that the Orange County median selling price in March of $1.2 million was a peak – tying a high set in May 2024.

Prices have risen 4.3% over 12 months, part of a 70% jump in the last six years.

Mortgage mania

The Fed’s move to raise interest rates helped to explode what house hunters pay.

In the three years of the central bank’s inflation battle, Orange County home prices rose 19% as mortgage rates soared to 6.7% from 4.3%. That created a 57% boost to a buyer’s estimated house payments.

Contrast those swings to the three previous years when coronavirus-spun rates gyrated from 4.3% to a historically low 2.9% back to 4.3%. Home prices rose 43% with only a 42% payment jump.

Who can afford this?

Rising home prices aren’t a sign of market strength. They’re the reason why homebuying is frozen.

Over six years, an Orange County buyer’s typical mortgage check increased by 122%. In that same period, there was only a 25% increase in Orange County incomes.

So, what would it take to close the affordability gap? My spreadsheet suggests 44% price cuts, 1.8% mortgages, or 77% pay hikes. Or a mix of the trio.

Then eyeball the budget-busting fallout this way.

Only 12% of Orange households could qualify to buy in 2025’s first quarter, according to calculations from the California Association of Realtors.

Six years earlier, this affordability yardstick showed 24% could buy – and this qualification measure has averaged 21% since 2006.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at jlansner@scng.com