What’s the difference between the homebuying tumble of the past three years in Orange County and the Great Recession’s infamous crash?

My trusty spreadsheet looked for clues in 21 years of sales stats from Attom tracking closed deals for houses and condos, existing and newly constructed. The deep reluctance of house hunters to buy in 2023 and 2025 was compared to the ugliness of the 2007-2009 debacle.

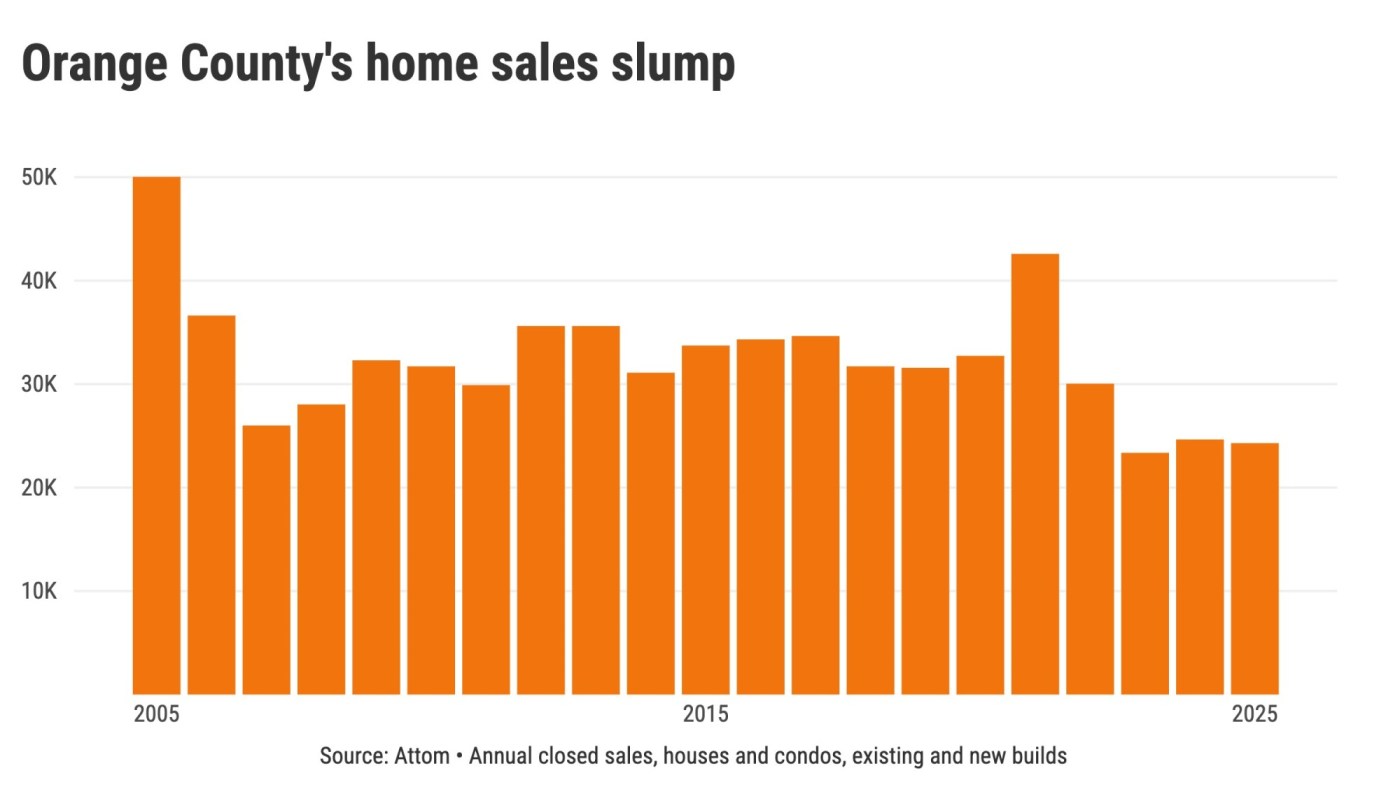

Consider how far sales have fallen recently.

Orange County had 72,305 sales in 2023 through 2025 vs. 86,339 in 2007-2009. So, recent homebuying was 16% slower the past three years than during housing’s nightmare period.

Yes, far fewer homebuyers these days than during the big crash. And the sales drop was 25% across six Southern California counties.

Next, contemplate the contrasting moves in home prices – noting the difference in housing’s economic backdrop: the recent post-pandemic economic unrest to 2007-2009’s global financial meltdown.

In Orange County, the $1.15 million median home price for December 2025 was 23% higher than three years earlier – and just 5% below its all-time high.

That’s far different than the 31% price slashing in the three years ending in December 2009.

The monthly payment

Now, let’s talk affordability. For starters, think about the gyrations of mortgage rates.

Over the last three years, the Federal Reserve battled surging inflation by raising interest rates. That meant Freddie Mac’s average 30-year mortgage rate rose from 6.3% at the start of 2023 to 7.6%, then dropped to 6.2% by December 2025 as inflation finally cooled.

Back in those Great Recession years, the Fed juggled a global economic meltdown. Home loan rates fell from 6.2% in January 2007 to as low as 4.8% as the financial crisis spiraled out of control. The rate was 4.9% in December 2009.

Finally, meld those rate swings with price moves to see a key difference in the home-shopping climate during these two extremely sluggish periods.

Ponder a typical buyer’s estimated monthly house payments. An Orange County house hunter’s financial burden rose 17% in the past three years, while house payments tumbled 40% in 2007-2009.

It’s those deep discounts that got house hunters into a buying mood as the Great Recession’s crash unfolded.

What’s next?

Does the pain of 2007-2009 offer any hints about how quickly homebuying can shake off significant blows?

Even with dramatically improved affordability, Orange County’s rebound from the Great Recession’s troubles was lethargic.

Over the next three years, sales grew by 13% while home prices recovered by 9% through the end of 2012.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at jlansner@scng.com